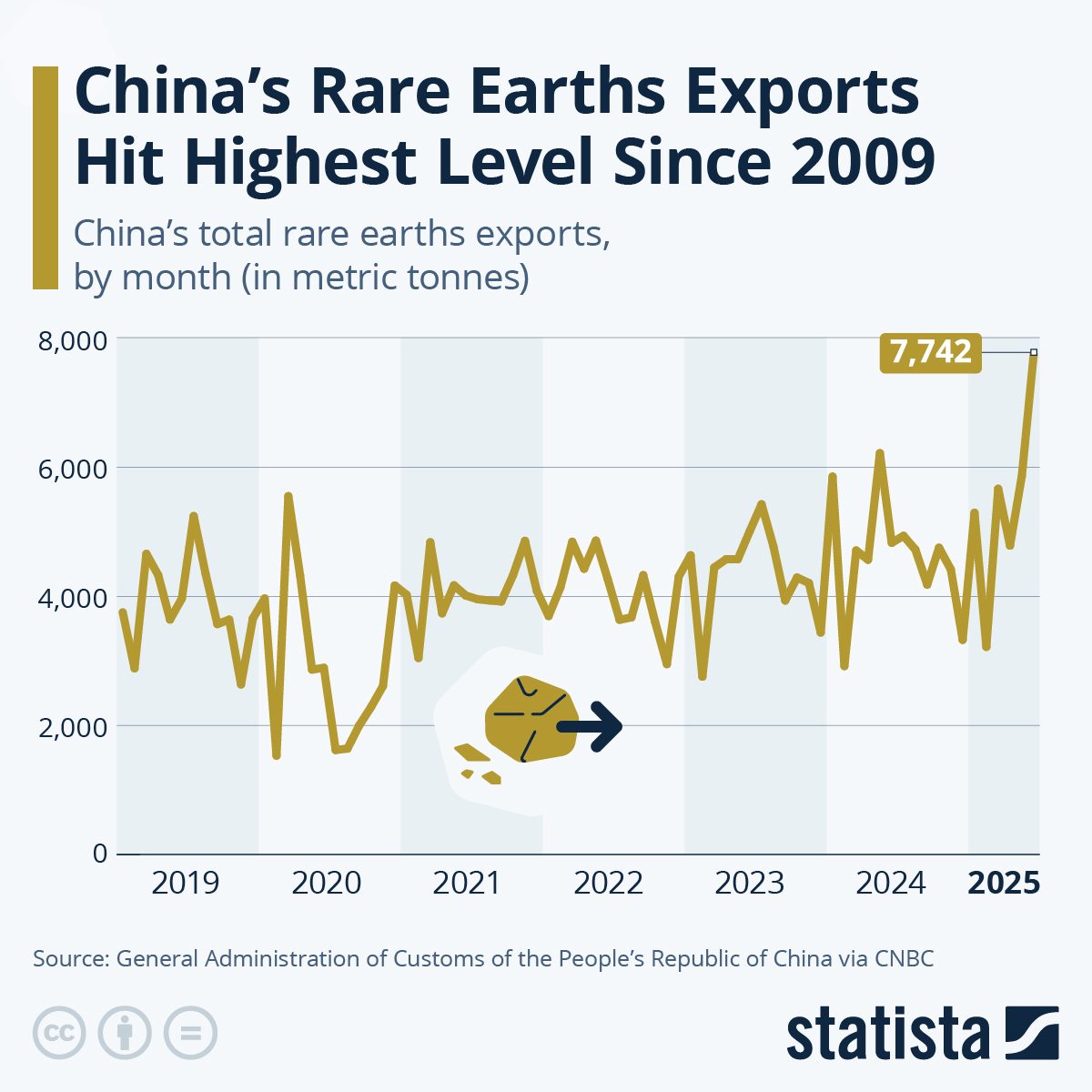

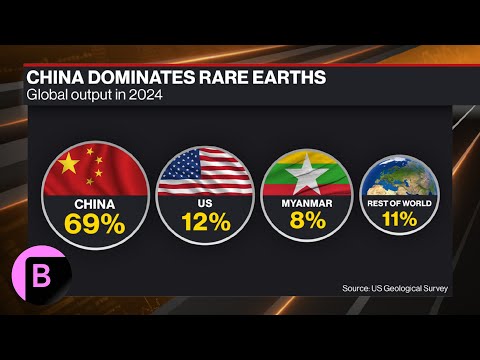

The United States imports roughly 80% of its rare earth elements and relies on China for over 90% of processing—materials essential to electric vehicles, wind turbines, and precision weapons. China's April 2025 export controls on seven heavy rare earths remain in force, with a broader set of restrictions due to expire in November 2026.

The Trump administration launched a $12 billion strategic mineral stockpile and a 55-nation Critical Minerals Ministerial in February 2026, producing 11 bilateral supply agreements and the FORGE coalition. MP Materials posted 49% revenue growth in Q1 2026, Lynas signed a $96 million Pentagon offtake deal in March, and USA Rare Earth struck a $2.8 billion deal to acquire Brazil's Serra Verde. At the Trump-Xi Beijing summit in May, China pledged to address specific element shortages but made no formal commitments, with the Section 232 deadline arriving July 13.

Why it matters

Chinese export controls can freeze weapons programs, stall EV production, and wipe out industries—proving America can't make anything without these materials.

28 events

Latest: May 28th, 2026 · 4 weeks ago

Showing 8 of 28

JK to step

Tap a bar to jump to that date

Jump to

May 2026

MP Materials Sues USA Rare Earth Over Magnet Trade Secrets

LatestCorporate

MP Materials filed suit in Texas federal court alleging a former employee stole proprietary "grain boundary diffusion" magnet formulations and shared them with USA Rare Earth and a third-party firm. Both companies receive federal backing, making the dispute a government-funded rivalry; USA Rare Earth denied all allegations.

DOE Awards $45.7M for 19 Critical Minerals Projects

Funding

The DOE Office of Critical Minerals and Energy Innovation announced $45.7 million across 19 projects to fill domestic supply chain gaps, including pilot-scale facilities for rare earth and magnesium processing. Awardees include Argonne National Laboratory, Columbia University, and Ohio University.

Trump-Xi Beijing Summit Produces No Rare Earth Deal

Geopolitical

President Trump traveled to Beijing for a summit where rare earth access was central to the agenda. China agreed to "address US concerns" on yttrium, scandium, and neodymium but made no binding commitments and left the April 2025 controls on seven heavy rare earths fully in place.

March 2026

Lynas Signs $96M Pentagon Rare Earth Offtake Deal

Corporate

Lynas Rare Earths signed a binding letter of intent with the US Department of War to supply rare earth oxides for $96 million over four years at a $110/kg NdPr floor price. The deal replaces the original Texas refinery plan, which Lynas confirmed is unlikely to proceed.

February 2026

US Announces Critical Minerals Trading Bloc

Policy

Trump administration unveils plans for allied trading bloc (EU, Japan, Mexico) with price floors maintained via tariffs to counter China dominance and secure rare earth supply chains.

US Hosts Critical Minerals Ministerial, Launches FORGE Coalition

Policy

Secretary of State Rubio convened 55 foreign delegations in Washington and signed 11 bilateral supply agreements. The meeting launched FORGE (Forum on Resource Geostrategic Engagement), a successor to the Minerals Security Partnership chaired by South Korea, designed to coordinate price floors and counter Chinese market dominance.

Rare Earth Stocks Surge on Trading Bloc News

Market

US rare earth miners rally—Critical Metals +10%, USA Rare Earth +11%, MP Materials +4%—following critical minerals trading bloc announcement and Project Vault momentum.

Trump Launches $12B Project Vault Stockpile

Policy

$12B strategic critical minerals reserve ($10B EXIM loan + $1.67B private) including rare earths, modeled on Strategic Petroleum Reserve; GM, Boeing, Google commit.

January 2026

DOE Application Deadline Closes

Milestone

Final deadline for applications to $134 million rare earth demonstration program. Awards of $67-134M each expected for up to 2 projects; selection anticipated February 2026.

Trump Signs Critical Minerals Executive Order

Policy

President Trump invokes Section 232 national security authorities, ordering Commerce and USTR to negotiate critical minerals trade agreements with 180-day deadline. Failure triggers potential tariffs or minimum import prices.

MP Materials CEO Sells $19.2M in Stock

Corporate

James Litinsky sells 300,000 shares at approximately $64 per share via pre-arranged trading plan. Stock up 33% year-to-date amid government partnership and production ramp-up.

China Bans Rare Earth Exports to Japan

Geopolitical

China halts rare earth and magnet exports to select Japanese firms following Prime Minister Takaichi's comments on potential military intervention in Taiwan Strait conflicts. Japan relies on China for 63% of rare earth imports.

December 2025

DOE Announces $134M Demonstration Program

Funding

Department of Energy opens applications for Rare Earth Elements Demonstration Facility program targeting recovery from unconventional feedstocks.

November 2025

China Suspends October Controls for One Year

Geopolitical

Following US-China negotiations, China suspends October export controls until November 2026. April 2025 restrictions on heavy rare earths remain in place.

October 2025

Phoenix Tailings Opens First US Metallization Facility

Milestone

Exeter, New Hampshire facility begins producing 200 tons/year of rare earth metals with capacity to scale to 1,000+ tons—enough to supply entire US defense industrial base. First domestic rare earth metallization without Chinese inputs.

China Escalates with October Controls

Geopolitical

China announces expanded export controls including extraterritorial provisions requiring licenses for products made outside China using Chinese rare earth materials.

July 2025

Apple Announces $500M MP Materials Partnership

Corporate

Apple signs long-term agreement with MP Materials for American-made rare earth magnets from recycled materials, expanding domestic supply chain commitments.

DOD Takes 15% Stake in MP Materials

Investment

Pentagon invests $400 million equity in MP Materials, becoming largest shareholder. Deal includes $150M loan, 10-year offtake agreement, and $110/kg price floor—triple market rates.

May 2025

US Rare Earth Imports Collapse

Trade

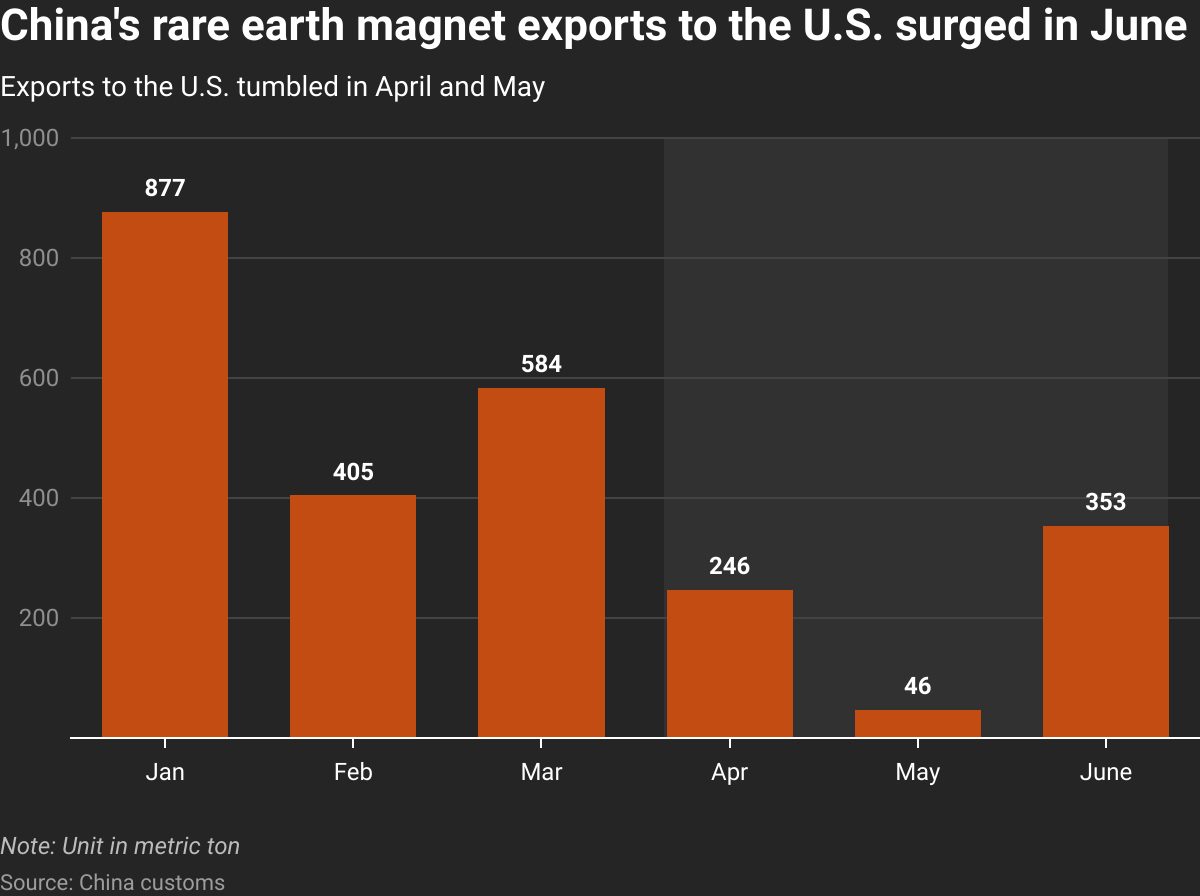

Chinese rare earth magnet exports to US fall 93.3% year-over-year. Ford temporarily closes Chicago factory; automakers scramble for supply.

April 2025

China Imposes Rare Earth Export Controls

Geopolitical

China requires export licenses for seven heavy rare earth elements—including samarium and dysprosium—in response to US tariffs. Defense contractors effectively barred from purchasing.

April 2022

DOD Awards MP Materials $35M

Funding

Department of Defense awards contract to MP Materials to design and build heavy rare earth separation facility at Mountain Pass.

November 2021

Bipartisan Infrastructure Law Enacted

Policy

President Biden signs legislation including $140 million for DOE rare earth demonstration facilities and over $600 million for critical mineral programs.

June 2017

MP Materials Acquires Mountain Pass

Corporate

Consortium led by JHL Capital purchases Mountain Pass mine at bankruptcy auction for $20.5 million, beginning revival of US rare earth production.

June 2015

Molycorp Files for Bankruptcy

Corporate

America's only major rare earth producer files Chapter 11 with $1.4 billion in debt. Mountain Pass mine shuts down as rare earth prices collapse from post-2010 highs.

August 2014

WTO Rules Against China

Legal

WTO finds China's rare earth export restrictions violate trade rules. China subsequently drops export quotas in 2015.

March 2012

US Files WTO Case Against China

Legal

United States, Japan, and European Union jointly file WTO dispute against China's rare earth export restrictions.

September 2010

China-Japan Rare Earth Crisis Begins

Geopolitical

Chinese fishing trawler collides with Japanese Coast Guard near disputed Senkaku Islands. China halts rare earth exports to Japan for two months, triggering global price spike and supply chain panic.

Historical Context

3 moments from history that rhyme with this story — and how they unfolded.

After Japan detained a Chinese fishing captain near the disputed Senkaku Islands, China halted rare earth exports to Japan for approximately two months. Japan imported 90% of its rare earths from China. Prices for some rare earths spiked over 2,000%—the cost of US rare earth imports rose from $6,969 to $170,760 per metric ton by 2011.

Then

Japan's automotive and electronics industries faced immediate supply disruptions. The crisis triggered a global rare earth price bubble lasting through 2011.

Now

Japan invested 100 billion yen in supply chain resilience, cutting China dependence from 90% to 60% and halving total rare earth consumption through efficiency and recycling. Lynas received $250 million in Japanese investment. The WTO ruled against China's export restrictions in 2014.

Why this matters now

The 2010 crisis demonstrated China's willingness to weaponize rare earth supply. Japan's response—diversification, efficiency improvements, recycling, and allied investment—provides a template for US strategy. The current situation is more severe: April 2025 restrictions target defense applications specifically.

2 of 3

June 2015 - June 2017

Molycorp Bankruptcy and Mountain Pass Collapse (2015)

Molycorp, America's only major rare earth producer, filed Chapter 11 bankruptcy with $1.4 billion in debt. The company had invested over $1 billion to modernize Mountain Pass after the 2010 price spike, but prices collapsed before full production began. Shares fell from $79.16 to $0.35. The mine sold at auction for $20.5 million.

Then

The US lost its only significant rare earth production capability. Mountain Pass sat idle for two years.

Now

MP Materials acquired and revived the mine, going public in 2020 at a $4 billion valuation. The experience demonstrated both the volatility of rare earth markets and the difficulty of competing with Chinese state-subsidized production.

Why this matters now

The Molycorp failure shows why government support—like the July 2025 DOD price floors—may be necessary to sustain domestic rare earth production. Private capital alone proved insufficient against Chinese market manipulation.

3 of 3

October 2010 - Present

Japanese Rare Earth Strategy (2010-2025)

After the 2010 embargo, Japan launched a comprehensive five-pillar strategy: reduce rare earth usage through technology, develop substitute materials, promote recycling, diversify suppliers, and build strategic stockpiles. The government invested 100 billion yen ($1.2 billion) immediately. State-backed entities invested $250 million in Lynas, securing 30% of Japanese demand.

Then

Japanese companies rapidly developed motors using fewer rare earths and found substitutes for some applications.

Now

Japan cut China dependence from 90% to 60% while halving total consumption. The Lynas investment helped create a second major non-Chinese rare earth producer. Japan's approach became a model for resource security policy.

Why this matters now

Japan achieved meaningful diversification in 15 years through sustained government-industry coordination. The US is attempting a similar effort but started later. The DOE demonstration program and DOD's MP Materials investment mirror Japan's playbook.